22 Jun Study on alternative management in Europe Part 2

A brief history of Alternative Investments in Europe

Traditionally, it has always been said that a financial portfolio should be composed and diversified between positions in cash, fixed income and stocks and, until recently, there was not even possible to include other types of assets in them. In recent years, it has become more and more common for investors to invest a part of their portfolios in alternative investments.

The long period of low interest rates that Europe is facing as a result of the accommodative policies of central banks (see Chart 5), puts conservative investors in front of a big dilemma and decision: to take more risk in the stock market (with increasingly adjusted valuations) in order to continue with the same level of profitability initially set as a target; or to assume that in the coming years they may incur losses and decrease their purchasing power if they maintain their positions in fixed-income assets. Therefore, alternative strategies are becoming increasingly popular for investors, who must look beyond traditional assets.

Chart 1: Evolution of deposit rates of Spanish entities.

Source: Investment in alternative assets, September 2019. AFI and Aberdeen Standard Investments.

It should be added that until the subprime crisis erupted, alternative management had remained in the offshore (or unregulated) world. But in a context of interest rates such is the current one, alternative management has been considerably democratized and regulated. Although it is a mature market, it is almost unknown to many investors due to the lack of regulation and official figures that only recently allowed a global and homogeneous view of the industry.

In line with this idea, it can be added that, according to Funds Society, in 2012, the ratio between UCITS funds and alternative funds was 70-30%, respectively, and only 6 years later is 60-40%[1]. The AIFMD directive has contributed to this growth.

Firstly, as far as geographical distribution is concerned, the United States remains the world reference country in this industry, but its importance has been reduced in recent years in favor of other areas such as Europe.

Indeed, the growth of the European alternative management industry in the last few years, both in terms of the number of institutions and the number of assets managed, has been considerable, given the impetus and prominence that the Hedge Fund funds have had in particular[2].

Chart 2: Growth in assets under management by asset class

Source: World Economic Forum Investors Industries into “Alternative Investments 2020: An Introduction to Alternative Investments”).

Within Eurozone countries, 90% of alternative assets under management are concentrated in Germany, Ireland, France, UK and Luxembourg. The majority of the funds (76%) are distributed across the EEA.

Chart 3: Concentration of AIFs in a few countries

Source: ESMA Annual Statistical Report on EU Alternative Investment Funds 2020

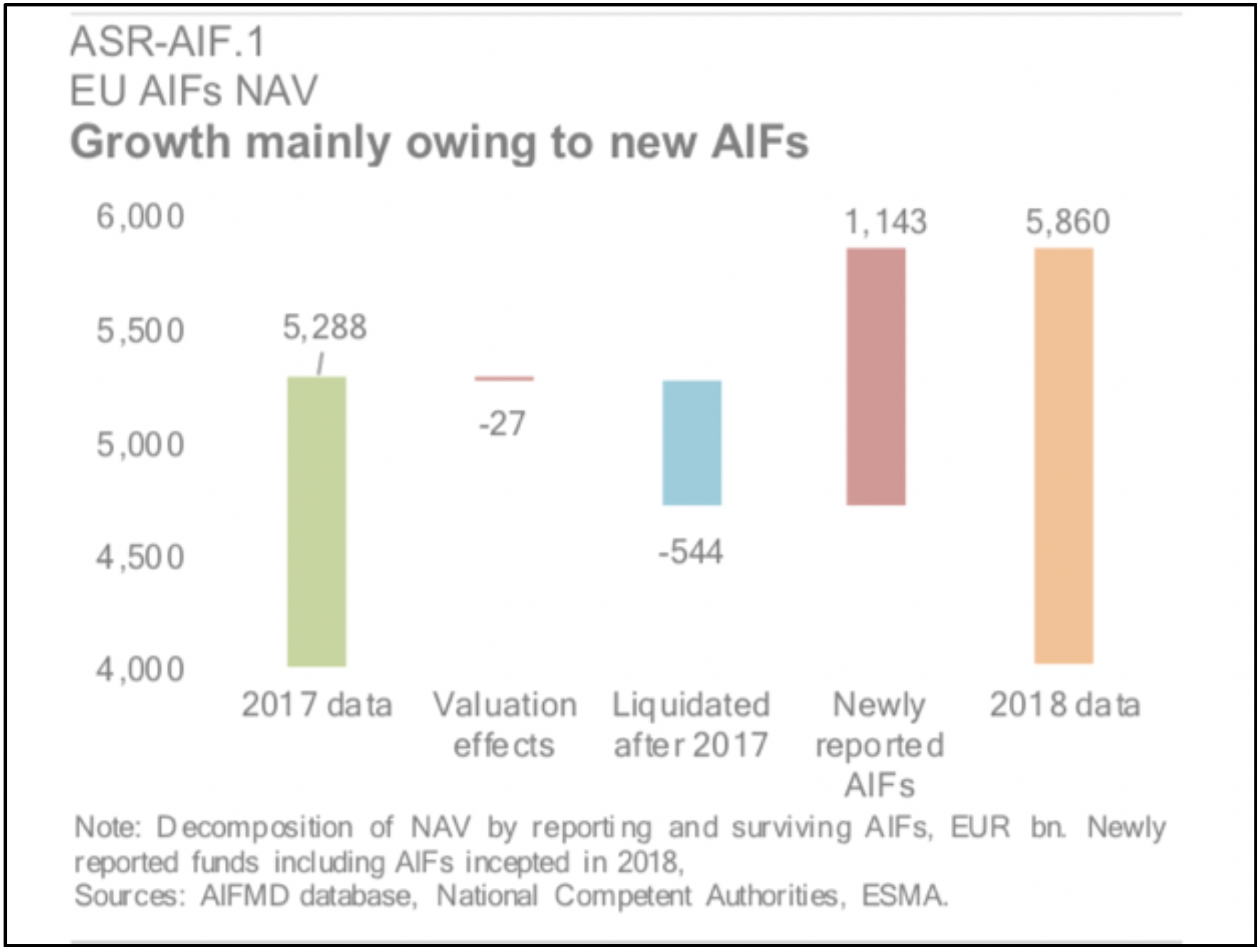

The current European alternative management industry is made up of more than 10,000 managers who manage approximately 5.8 trillion euros (figures at the end of 2018) with annual growth of 10% as a result, in large part, of the increase in creation of new investment funds (see Chart 8). With its growth in recent years, alternative management funds account for 40% of the investment fund industry in Europe (up from 33.4% in 2017)[3] and 20% of alternative management assets globally[4].

Chart 4: Growth mainly owing to new AIFs

Source: ESMA Annual Statistical Report on EU Alternative Investment Funds 2020

Chart 5: Alternative investments by region

Source: Prequin Markets in Focus: Alternative Assets in Europe, June 2018.

As for their concentration, the market is distributed in few, but large investment funds that concentrate almost the entire market share of assets under management. According to ESMA, “In 2018, AIFs with a NAV larger than EUR 1bn accounted for less than 5% of all AIFs but more tan 55% of the NAV. Smaller AIFs (NAV lower than EUR 500mn) account for 93% of all AIFs but only 32% of NAV)”.

Chart 6: High concentration among a few latge AIFs

Source: ESMA Annual Statistical Report on EU Alternative Investment Funds 2020

As far as the type of investor is concerned, the professional investors represent 84%, among which pension funds or insurance companies are the main ones, accounting for 28% and 16% respectively of the total managed assets. Banks account for 7% and other institutional funds or clients for 8% each. As for the retail investor, its share is smaller and stands at around 16% (31% of which invest in fund of funds).

According to ESMA, funds of funds accounted for 14% of the industry, followed by Real Estate Funds (12%), Hedge Funds (6%) and Private Equity Funds (6%). The remaining category of other AIF accounts for 61% of the industry, covering a range of strategies with fixed income and stocks.[5]

Chart 7: AIF industry by type

Source: ESMA Annual Statistical Report on EU Alternative Investment Funds 2020

Chart 8: Crecimiento de volumen por tipo de activo

Source: Guide to Alternatives (J.P. Morgan Asset Management)

Conclusions

In Laurion we are aware that there are countries where the financial culture is scarce in terms of alternative investment, since it is relatively new in Europe, as we have seen.

We are also conscious of the need for many institutional and qualified investors to gradually incorporate alternative assets into their portfolios other than the traditional ones.

At present time, where volatility indexes are at record highs and interest rates at lows and with no prediction to change that in the near future, it is particularly important to raise awareness for the possibility of valuing alternative investment as a long-term investment solution.

As we have commented before, traditional investment has changed in recent years and needs to be complemented with alternative assets that bring profitability, security, stability and added value to traditional portfolios. It should not be forgotten that alternative investment is part of our real economy and it needs to continue to grow for the sustainability of the financial system and the circular economy itself.

[1] “Alternative investment gains strength as a way to overcome the profitability challenge», KPMG, published on Tuesday 25 February 2020 in Funds Society www.fundssociety.com.

[2] CNMV, Study on hedge funds industry

[3] ESMA Annual Statistical Report on EU Alternative Investment Funds 2020

[4] Prequin Markets in Focus: Alternative Assets in Europe, June 2018

[5] ESMA Annual Statistical Report on EU Alternative Investment Funds 2020